1) US

WW 2 foodstuffs and arms to the Axis

grew the economy and moved most Axis gold to the U.S.

2) Gold was valued at $35 per ounce

and after the war, other currencies were a little undervalued in terms of gold. This

allowed

countries to sell natural resources and the few goods they produced to the

large U.S. market at low prices. 3)

U.S. manufactures didn't mind because England, France,

Germany and Japan had lost much of their industrial base and produced

little for export. With little world competition U.S. exporters had

Oligopoly power. This power allowed U.S. exports to be priced at a

relatively high price resulting in high profits for US companies and

high salaries for

workers. 4)

US loaned dollars to

exporting nations which were returned for high quality U.S.

manufactured goods plus private and public financial assets.

5)Eventually the Marshal Plan

added even more dollars into the world currency system which also flowed back to the US.

And only the U.S. could print dollars.

This was acceptable as long as the US could convert

dollars to gold at $35 per ounce. This dollar exchange standard

worked for two decade.

2. The value of the convertible

dollars became problematic during the 1960's because of these US deficit

problems.

President

Johnson's war on poverty:

Job training, Direct Food Assistance

and Direct Medical Assistance for about four million poor people. Specific programs include

Head Start, Job Corps, Food stamps,

Medicaid, Student Financial Aid.

Vietnam War borrowing

cost of $500 billion

and

Countries were unhappy

using the U.S. dollar. Why?

3. The US gold reserve of $30

billion were already backing much more in existing dollars

and the U.S. government refused to raise

taxes to

slow US economic activity, slow inflation and protect the dollar.

US inflation put international pressure on the dollar which caused

massive gold outflows. This resulted in the

Nixon Shock

which severed the dollar link to gold and eventually creating a

floating value for gold. The US thus hadfiat money

system. A new negotiated gold value for the was needed.

4. To cushion the shock on U.S.

exporters,

a 10% surtax on all imports was instituted.

Britain continued to prop up the

pound against a currency market that clearly wished a lower value.

Markets simply did

not want Britain's prestigious value, yet successive

Chancellors* fearing a sterling collapse, refused to allow it to float freely.

In 1976, the Chancellor of the Exchequer called in the IMF to help

arrest persistent runs on sterling. On the advice of the IMF, the

Chancellor imposed austerity measures, which reduced inflation and

improved economic performance. The IMF’s loan was never fully drawn. The

pound recovered – but only temporarily. Against a background of rising

unemployment, the famous “Winter of Discontent” of 1978 sounded the

death knell for the Labor government. In 1979, the Conservatives under

Margaret Thatcher won the election.

Many fear U.S. debt may cause the US dollar to have the same

fate.

Japan soon increased the Yen's

value against the dollar by 7% meaning the US dollar price of Japanese

goods had increased by 17%. Others would be forced to follow. Eventually

individual countries negotiated an increase of the dollar value of their

currencies by 3% to 8% depending on their US negotiation power. The

dollar price of gold was also increased by 9%. So US imports became more

expensive by 12% to 17% and import prices decreased by the same amount.

In 1973 the value of the weaker dollar was set at $42 and then allowed

to float with other currencies. This meant Bretton Woods

finally collapsed.

Nixon was happy because printing dollars to pay for stuff was

now allowed. No gold needed.

5. Nixon also abolished the

International Monetary Fund’s international capital constraints

that

had allowed Arab oil producers to recycle

their petrodollars into New York banks. The global ‘Petrodollar’

was born and the overseas dollar was becoming the world's currency.

This massive invasion of petro dollars into the US Banking

System would end up in a world economy that really didn't need them.

Easy money was here to stay. Deep-Do-Do would result from

international loan bad debts.

Advantages of

overvalued dollar for U.S. were cheap energy, cheap imports including

foreign travel, low interest rates on all US debt including mortgages

and cheaper foreign expansion by US companies.

Disadvantage is high valued dollar hurts

competitiveness of U.S. exporting companies, companies that compete with

imports and anyone working for these companies.

In 2016 the US,

a debtor nation brought in $180 billion more than it paid out.

China, a creditor nation paid out $50 billion more. source

What’s good for the global economy (and for many Americans)

is bad for U.S. manufacturers

and their workers as their products suffered a permanent price disadvantage. For them, the

global dollar is not a privilege. It’s a stubborn curse. Since 1976, the

United States has not had one annual trade surplus. The New Normal of ever

increasing manufacturing wages was over, another

New Normality had begun. It’s

trade deficits were not the result of poor U.S.

competitiveness. In reality,

our deficits were required to supply the world with a currency

for international trade and investment.

The many advantages of

being the world's currency would continue and politicians began

looking for solutions to work force problems caused by

Free Trade.

SourceReadings

Editor's Note: While most of this by political

Trump's posturing and return posturing by our economic

adversaries. Foreign leaders posturing began when

de Gaulle threw a fit. See

Russia, China Rivals or Adversaries?

U.S. companies are warning that currency

fluctuations are weighing on their results,

raising a red flag for investors heading into the thick of the

second-quarter earnings season, Akane Otani reports.

A weaker dollar benefits U.S. multinationals by making exports cheaper to

foreign buyers and also making their overseas profits look bigger when

translated back into the U.S. currency.

But

strong economic growth, stable inflation and the Fed's plan to gradually

raise short-term interest rates is boosting the greenback. The

WSJ Dollar Index, which gauges the U.S. currency against a basket of 16

others, rose to 88.63 Tuesday, its highest level in more than a year.

U.S. friends and foes, looking

to buck American control over international trade, are

developing alternative systems.

The catalyst was the Trump

administration’s decision to again impose trade sanctions on Iran,

Justin Scheck and Bradley Hope report.

The

U.K., Germany and France are fine-tuning a system to enable

trade with Iran without using dollars.

India

wasn’t happy either. It began using a similar

alternative system in November.

China

and Russia are striking deals to trade with yuan

and rubles instead of dollars.

Global

trade runs on dollars and resulting clout has long made allies

and enemies vulnerable to U.S. trade sanctions. Dollar’s dominance

will continues but recent reactions to Trump may diminish the U.S.’s power to impose its policies.

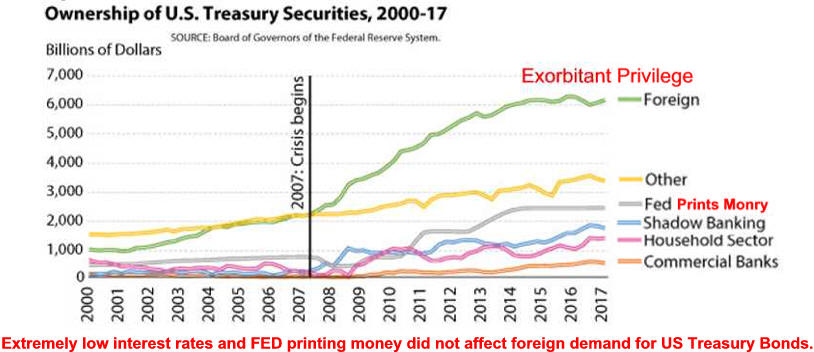

Exorbitant Privileges

Continues because

the dollar has not faced any

significant competition from the Japanese Yen, English

Pound , Euro, and Chinese Renminbi because of their weak

economies and weak government in relation to US. The Special

Drawing Rights (SDR)

system of the International

Monetary Fund has not gained traction. For now, no

alternatives exist.

Current system is unsustainable according to those experts

believing the system favors the United States too much.

Alternatives will emerge to correct imbalance existing since

the 1971 Nixon shock.

Source

In 1971, Nixon suspended convertibility of the dollar to gold,

effectively ending the Bretton Woods system. But even after this, Dollar Privilege Continued.

Loss of U.S. economic dominance has

been aided by Trump's lowering our place as Leader of the

Free World. This when the U.S. dollar continues its dominate

role as does American Exceptionalism.

The European Central Bank the dollar makes up

two-thirds of both international debt and global reserves.

Oil and gold have long been priced in dollars. Iran, North

Korea, and Russia and other developing are terror stricken

by the loss of dollar needed to finance the global payments

system.

The dollar hegemony may be weakening.

Political leaders are pushing back. Paying for European

goods bought from European companies should be in

Euros, not dollars. China recently challenged the dollar

supremacy with a

Yuan-based

oil futures contract Russia all

but eliminated

her US dollar based investments

because she perceived wreaking

dollar.

Upsetting US Actions

Pressuring non-US companies trading with Tehran.

Editor's Note: While most of this by political

Trump's posturing and return posturing by our economic

adversaries. Foreign leaders posturing began when

de Gaulle threw a fit. See

Russia, China Rivals or Adversaries?

The Dollar

May Be Knocked off Its Pedestal

America’s competitors, friend and foe

, have opportunities

to challenge the U.S. currency.

By

Sahil Mahtani

The consensus answer of

no is too complacent.

Developments in foreign-exchange markets during

the past 18 months point toward dedollarization.

1. Chinese “petroyuan” crude-oil futures, launched

last year in Shanghai, now sits right behind Brent and West Texas

Intermediate in trade volume.

2. The world’s central banks bought more gold last

year than at any time since President Nixon took the U.S. off the gold

standard in 1971.

3. Markets recently learned that China added gold to

its reserves for the fifth month in a row.

4. U.K., France and Germany created a new

payment-processing system to permit payments to Iran.

5. Russia shifted $100 billion of dollar-denominated

reserves into Chinese yuan, Euros and Japanese yen, as it did last year.

Presidents Obama and Trump increase in sanction is

the immediate cause of dedollarization.

1. Braking US

sanctions on Iran and Cuba cost French bank

BNP Paribas a $8.9 billion US Justice Department fine in 2014

plus a one-year suspension in use of US international banking system.

2. European Commission President said: “It is

absurd that European companies buy European planes in dollars instead of

Euros.”

3. As America buys less international crude oil and

the Chinese buys more, oil exporters may begin to accept other

currencies. Oil companies in Russia, Iran and Venezuela have already

begun accepting yuan. Were Saudi Arabia to join them, the effects could

be substantial.

4. Political polarization, continuing tax cuts and an

expanding federal safety net mean increased U.S. fiscal and current

account deficits which are a good leading indicator, with a

two-year lag, of dollar weakness.

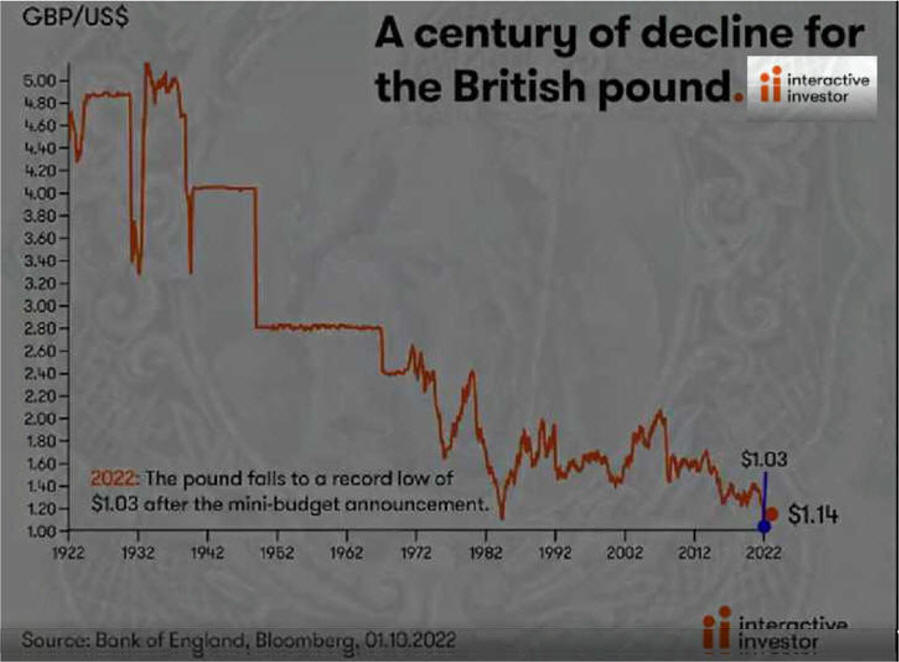

By the early 1970's, the pound sterling, once the

world's proximate reserve currency, accounted for just under a third of

global sovereign reserves. By the end of that turbulent decade, it was

less than 1/20th.

Persistent talk of a shift away from the dollar began

in the 1970s, but habitual dollar use remains high—everywhere.

Nevertheless, the emergence of a genuinely multi-polar world,

[which America First will accelerate]

means the coming market cycle is likely to be different. The U.S. dollar

may finally be knocked off its pedestal.

Mr. Mahtani is a strategist at Investec Asset Management

"(Bloomberg Opinion) -- Convinced of an

existential threat from competitors, America is weaponizing the

dollar to preserve its global economic and geopolitical

position.

History

While the U.S. accounts for about 20 percent of

the world’s economic output, more than half of all global

currency reserves and trade is in dollars. This is the result of

the 1944 Bretton Woods agreement, the effect of which was

enhanced when the link between the dollar and gold ended in the

1971 Nixon shock, allowing America to control the supply of the

currency.

The dollar’s pivotal role — an “exorbitant

privilege,” in the term coined by then French Finance Minister

Valéry Giscard d'Estaing in 1965 — allows the U.S. easily to

finance its trade and budget deficits. The nation is protected

against balance-of-payments crises, because it imports and

services borrowing in its own currency. American monetary

policies, such as quantitative easing, can influence the value

of the dollar to gain a competitive advantage.

But the real power of the dollar is its

relationship with sanctions programs. Legislation such as the

International Emergency Economic Powers Act, the Trading With

the Enemy Act and the Patriot Act allow Washington to weaponize

payment flows. The proposed Defending Elections From Threats by

Establishing Redlines Act and the Defending American Security

From Kremlin Aggression Act would extend that armory.

More Weapons

When combined with access it gained to data from

Swift, the Society for Worldwide Interbank Financial

Telecommunication’s global messaging system, the U.S. exerts

unprecedented control over global economic activity.

Sanctions target persons, entities,

organizations, a regime or an entire country. Secondary curbs

restrict foreign corporations, financial institutions and

individuals from doing business with sanctioned entities. Any

dollar payment flowing through a U.S. bank or the American

payments system provides the necessary nexus for the U.S. to

prosecute the offender or act against its American assets.

This gives the nation extraterritorial reach over

non-Americans trading with or financing a sanctioned party. The

mere threat of prosecution can destabilize finances, trade and

currency markets, effectively disrupting the activities of

non-Americans.

The risk is real. BNP Paribas SA paid $9 billion

in fines and was suspended from dollar clearing for one year for

violating sanctions against Iran, Cuba and Sudan. HSBC Holdings

Plc, Standard Chartered Plc, Commerzbank AG and Clearstream

Banking SA have paid large fines for similar breaches.

Secondary sanctions made it difficult for United

Co. Rusal to refinance dollar borrowings when global businesses,

banks and exchanges were forced to stop dealing with the Russian

company. Its bonds and shares plunged, even though the

company sells only 14 percent of its products in the U.S., does

not use American banks, and is listed in Moscow and Hong Kong.

ZTE Corp., a Chinese electronics company, was hit hard by the

inability to buy essential components from suppliers because of

sanctions for trading with North Korea and Iran. In these cases,

the entity was not in violation of laws where it was domiciled

or operated, and the proscribed acts took place outside the

U.S.

The Competition

China, Russia and increasingly Europe want an

alternative reserve currency system. The problem is that

immediate replacement of the dollar is difficult.

First, the euro, the yen, the yuan and the

ruble are not realistic options. The euro’s long-term future and

stability isn’t assured, while Japan’s economy remains trapped

in two decades of torpor. The Chinese and Russian political and

economic systems lack transparency, and the yuan isn’t fully

convertible.

Second, the required change in infrastructure is

daunting. Foreign-exchange markets where the dollar is the

currency of reference would have to be fundamentally

restructured. Deep and liquid money markets to support a reserve

currency can’t be conjured up overnight.

Third, most candidates are reluctant to take on

the role of a global reserve currency because of tensions

between national and global economy policy. The economist Robert

Triffin pointed out that the country whose medium of exchange is

the global reserve currency must meet external demand for

foreign exchange. This necessitates running large trade

deficits, requiring fundamental changes in the mercantilist

policies of Germany, Japan and China.

Conclusion

This means that the U.S. can continue to use the

dollar to help further its trade, financial and geopolitical

aims, largely outside the strictures of international laws and

institutions and without the need for messy, unpredictable

military campaigns. As John Connally Jr., Richard Nixon’s

Treasury secretary, put it in 1971: The dollar is “our currency,

but your problem.”

To contact the author of this story: Satyajit Das at

sdassydney@gmail.com

To contact the editor responsible for this story:

Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion

of the editorial board or Bloomberg LP and its owners.

Satyajit Das is a former banker whose latest book is

"A Banquet of Consequences." He is also the author of "Extreme

Money" and "Traders, Guns & Money."

If

2020 confirmed one thing, it was the centrality of the dollar to the global

economy. U.S.

hegemony may already have passed us in a political

and strategic sense, but U.S. financial influence is proving more enduring.

This is reassuring in the sense that the U.S. Federal Reserve has once again

acted as a responsive and generous steward of the dollar-based financial

system. But it is also a cause of puzzlement and frustration.

While China and Russia experiment with alternatives to the

dollar-based payment system, in Europe the buzzword of the day is “strategic

autonomy.” Given the increasing aggression of Washington’s financial sanctions,

compounded by the capriciousness of the presidency of Donald Trump, this is

hardly surprising. It is an obvious reaction to the weaponization of

interdependence.

It is far

from obvious to critics that dollar hegemony is an

unalloyed blessing. Inequality, deindustrialization, and the loss of

well-paid and secure blue-collar jobs can all be blamed on the dollar’s strength.

In that sense, the dollar’s standing and Trumpian populism are not so much

contradictions as functionally interconnected.

One helped cause the other.

Little wonder that visionary investors such as Ray Dalio of

Bridgewater, the world’s largest hedge fund, advise anyone who will listen to

prepare for a future beyond the dollar. In explaining his determination to

backing China, Dalio points to the rise and fall of

other financial empires, a recurring

cycle that stretches back over half a millennium.

But are history’s lessons really that obvious? The dollar has

been prominent in the world economy for just over a century, a period in which

we have seen the largest explosion of population, economic activity, and state

violence to date, a complete rupture on many metrics with any previous epoch in

the history of our species. It’s fitting, therefore, that what we sometimes

describe as a dollar system is not so much a well-defined and clearly delineated

institution than a constantly evolving assemblage tracking the staggering

transformations of the real economy and the international power system.

Periods of coherence in which monetary and financial policy were neatly aligned

with the grand strategic posture of the American empire were brief.

Contradictions are the norm, and those of the current moment are by no means the

most egregious. It is a history punctuated by crises. Talk about the end

of dollar hegemony started half a century ago, in the 1970s, the period during

which Foreign Policy was founded. Yet the

dollar has continued to dominate the world economy.

What allows it to do so is improvisation and action on the part

of U.S. policymakers and businesses and the choices of their counterparts around

the world. In gauging the future of the dollar as the world’s key currency,

history should indeed be our guide. But not history in the sense of grand

lawlike cycles. Our world is too complex, too protean, too radical for that. The

history that we need to understand is a tangled skein of discreet actions and

innovations. It is a history of power and money, in which the future is not

foreordained but still very much in play

2

The sudden rise during World War I of the

United States as the world’s financial hegemon came as a shock. In the

diplomacy of the July crisis of 1914, America was less relevant than

Serbia. If you assumed that the war would be over by Christmas, as many did,

then economics was irrelevant to the war, too. By 1916, with the meat

grinders of Verdun and the Somme consuming men and materiel on an

unimaginable scale, it was clear that everyone in the world needed

dollars, the currency that offered access to the last great pool of raw

materials, industrial capacity, and labor that was not already mobilized for

the war. When the United States did eventually join the war, the result

was that taxpayers in Britain, France, Italy, and Russia ended up owing

taxpayers in the United States billions of dollars, a novel and toxic

combination.

But, Europeans, led by John Maynard Keynes,

together with cosmopolitan bankers on Wall Street requested debt forgiveness.

The less America asked for, the lighter the burden of reparations could be on

Germany; a revived Europe would be good for democracy and for business.

For the United States, designing the League of Nations was a

responsibility with rather little burden. But now it was being asked to

arbitrate real economic trade-offs between domestic and international interests.

It was a big request—one that forced the central problem of

20th-century hegemony squarely into view. For the United States, designing the

League of Nations was a responsibility with rather little burden. But now it was

being asked to arbitrate real economic trade-offs between domestic and

international interests.

In Britain’s Victorian heyday as guarantor of the

global financial order, the flow of funds from London to the rest of the world

was the equivalent of many Marshall Plans per year. But that was private money.

After World War I, it was taxpayers who were on the hook at both ends. The first

era of dollar preeminence was political through and through. And that didn’t sit

well with U.S. democracy.

Victorious but depleted after World War I, London now challenged

the Americans to join it in forgiving the debts of Russia, France, and Italy.

But Britain found no willing partners. With the Republicans ruling Washington,

not only did the United States refuse to make generous concessions on the war

debts; it returned to protectionism, raised barriers to immigration, and

savagely deflated its economy, sucking gold out of the coffers of central banks

around the world. Even if its former associates in the war wanted to pay their

war debts, it was virtually impossible for them to do so. Adding new private

loans from Wall Street on top of the wartime debts only compounded the problem.

The United States was conducting a perverse experiment in being both a global

creditor and running a trade surplus at the same time.

Isolationism doesn’t describe America’s failure in the interwar

period. The real problem was the incoherence of its engagement with the world, which left liberal elites in Europe and Japan who banked on the greater exercise

of American power cut adrift, prey to the pressures of unmanaged financial

markets and domestic political discontent. That was the backdrop of the slide

into authoritarianism of Italy, Germany, and Japan. By the early 1930s,

America’s financial policy was so egregiously incoherent that even France and

Britain defaulted on their war debts to the United States. Lend-lease, the

famous assistance program of World War II, was structured precisely to avoid the

issue of war debts arising again.

Note US then was like Germany today. She is a creditor nation

running a trade surplus.

In 1944,

the Bretton Woods conference laid out a new vision. It was supposed to

square the stability of fixed exchange rates anchored on the dollar, with

limited capital mobility for the useful purposes of trade and investment.

With the U.S. currency anchored on gold, and everyone else tied to the

dollar, the hierarchy was more explicit than ever before. It was not so much

a gold standard as one based on the dollar.

But Bretton Woods did not work and not because of American

profligacy—it was the reverse: a desperate global shortage of dollars. Given the

debilitated state of Europe’s economy after the war, even limited exchanges of

European currencies for dollars easily resulted in a run. That became evident in

the summer of 1947, when Britain, the only country to attempt to implement

Bretton Woods immediately after the war, suffered a debilitating crisis and fell

back into reliance on bilateral U.S. funding. A market-based remedy would

have been a giant devaluation of all European currencies, but amid rising

tensions with the Soviet Union, that was too risky. Instead, on a tide of

anti-communism, the U.S. Congress voted for the Marshall Plan—not so much a complement to

Bretton Woods as an admission of failure.

It was not until 1958 that the basic commitment of Bretton Woods

to convertibility of currencies for trade and investment purposes came into

effect in the Atlantic economy. The postwar crisis of universal dollar shortage

was finally over. Japan and the European economies were strong enough either to

earn dollars through exports to the United States or by trading with those who

did. Indeed, if the market had been allowed to set the price of the U.S.

currency, it would have trended down against those of the champion exporters,

Germany and Japan. But Bretton Woods was a system of fixed exchange rates.

Exchange controls prevented speculative attacks on the dollar.

SOURCE: EUROPEAN CENTRAL BANK AND INTERNATIONAL MONETARY FUND

If Japan and Germany had been willing to allow inflation at

home, that would have helped maintain balance. But Germany in particular

resisted that mechanism of adjustment. And to make matters worse, the system was porous.

Wall

Street and its allies in the U.S. Treasury never liked Bretton Woods. They would

have preferred the world’s currencies simply to adjust to whatever level markets

dictated, and they found allies in London, which, from the 1950s, played host to

an offshore market for dollar deposits, known as the eurodollar market. On the

basis of those deposits emerged a freewheeling market for cheap dollar credits.

This was attractive for borrowers of all kinds. The first big eurodollar deal

helped finance Italy’s new motorway system.

But the increasing flux of unregulated private funds challenged

the official currency pegs. It was clear that if the market had operated freely,

the dollar would have dropped hard. Tools such as central bank swap lines, which

were to come back to the fore during the 2008 financial crisis, were first

pioneered in the 1960s to keep the Bretton Woods system afloat. Even in its

heyday, dollar hegemony was something of a Rube Goldberg contraption.

The anchor of the fixed exchange rate system was supposed to be

America’s fabled gold reserve at Fort Knox. But by 1970, the year when Foreign

Policy was founded, just $11 billion in gold backed $24 billion in dollar

exchange reserves held outside the United States. Clearly not every one of those

paper dollars could be cashed for gold. The dollar-gold peg was a convenient

fiction. When, in 1965, France began exercising its right to exchange dollars

for gold, it was met with accusations of

extortion from America. To maintain the official price of $35 per ounce of gold,

the U.S. government suppressed private gold purchases for much of the 1960s. It

was better not to know what the dollar was really worth.

In August 1971, U.S. President Richard Nixon announced that the

United States was ending convertibility of the dollar. When he was warned that

this move might shake the confidence of Cold War allies in Europe, particularly

Italy, Nixon responded,

“I don’t give a shit about the lira.”

4

And so

the modern era of fiat money was born. For the first time in history, no

currency in the world was tied to gold or any other metallic standard. The

value of money would rest purely on the authority of the state as judged by

markets. And the verdict seemed clear. The dollar plunged in value, giving

American exporters a much need fillip. Japan and Germany faced the surge in

their currencies they had long resisted. In the Winter 1971-72 issue of Foreign

Policy, one article was headlined, “How the Dollar Standard Died.”

As the dollar slid against the Deutsche mark and the yen, that

meme would circulate ever more widely. The modern system of summitry around the

Group of 7 nations was created to help manage the resulting pressures. Fearing

for his country’s exports, Helmut Schmidt, Germany’s ferocious chancellor of the

1970s, demanded that U.S. President Jimmy Carter put America’s house in order to

stop the dollar’s relentless slide. OPEC began considering whether to price its

oil on a more reliable currency. The Special Drawing Right, the synthetic

currency of the International Monetary Fund (IMF), was one option.

The first, and to date most serious, crisis of dollar hegemony

ended in October 1979 with Paul Volcker’s decision, as Federal Reserve chairman,

to allow interest rates to surge, sending a shock through the global economy.

That sent the dollar soaring. But more important than the steep ascent of the

dollar’s value was the mechanism by which the shock was transmitted: the ever

greater flux of hot money between the financial centers of the world.

After bursting the limits of Bretton Woods, liberalized currency

and financial markets boomed. And the dominant drivers of this new era of

financial growth were Wall Street banks, whether in New York or London. What

mattered was not the exchange rate of the dollar or formal arrangements of the

Bretton Woods type but the depth and sophistication of the financial markets

superintended by Wall Street. The center of foreign exchange trading may have

remained in London, and the value of the U.S. currency may have fluctuated, but

it was the dollar and the major American banks that were the pivot of every

trade.

The promise of this new order was flexibility, an efficient

reallocation of resources, and growth. In terms of GDP, the results were modest

compared with the golden age of the postwar period. But the financial boom was

huge. And this spilled over into a new wave of dollar-denominated international

lending. The upshot was more frequent and severer crises, not just of debtors

but of those who lent to them. The 1980s debt crises in Latin America were so

large that they jeopardized the U.S. banking system itself.

In Eastern Europe, the stability of the Soviet bloc was

threatened. By 1988, the communist

bloc owed $112 billion; the Soviet share alone was $28

billion. Moscow used much of the cash to pay for grain imports to offset the

failures of collectivized agriculture. But servicing the debts required a

surplus, and that meant squeezing the population. This was most dramatic in

Poland, the champion communist borrower, which came to owe $37.5 billion. In the

early 1980s, austerity policies by the communist regime triggered the Solidarity

trade union protests and the declaration of martial law.

The collapse of the Soviet bloc opened the door to a new era of

unipolar dominance by the dollar. There were parts of post-Soviet Eastern Europe

where Germany’s

Deutsche mark was the de facto standard, notably in war-torn

former Yugoslavia. But in general the greenback became king, the world’s de

facto global currency—even in Russia. When Vladimir Putin took power, the

Russian Treasury preferred to

have taxes paid in dollars.

5

At the

height of unipolar hubris, Time magazine

dubbed Fed Chairman Alan Greenspan, Treasury Secretary Robert Rubin, and

Deputy Treasury Secretary Lawrence Summers the committee to save the world.

That was grandiose. But the world did need saving. The debt crises of the

1980s blended into those of the post-Cold War period: first Mexico in

1994-1995, then the Asian economies in 1997, then Russia in 1998—which

spilled back to Wall Street by way of the hedge fund Long-Term Capital

Management—and finally the traumatic crisis in Argentina in 2001.

In trying to manage these shocks through a combination of new

loans, debt restructuring, and so-called structural adjustment, the U.S.

Treasury and the Fed faced constant resistance both from the victim countries

that railed at the infringement of their sovereignty and from a U.S. Congress

that resented aid for foreign countries. The European votes on the IMF board

carped that the whole regime only encouraged irresponsible financial expansion.

Not for nothing, Timothy Geithner, who cut his teeth in international financial

diplomacy as assistant secretary and undersecretary for international affairs in

the U.S. Treasury Department under President Bill Clinton (and would become

treasury secretary under President Barack Obama), would later describe the

efforts of those days as “defying gravity.”

The damage done to the legitimacy of debtor regimes such as

Suharto’s Indonesia and to the institutions through which the United States

acted, notably the IMF, was severe. The solution as far as many emerging markets

were concerned was to limit their exposure by cultivating sovereign borrowing in

domestic currency rather than dollars. The IMF’s client list shrank from year to

year as governments sought to avoid the odium of submitting to the Washington

Consensus. Beijing drew its own conclusions.

Undergoing a dramatic opening up and the transformation of its

economy, China was determined to avoid the fate of its emerging-market peers.

Undergoing a dramatic opening up and the transformation of its

economy, China was determined to avoid the fate of its emerging-market peers. It

pegged its currency to the dollar at an undervalued rate, used exchange controls

to regulate the flow of funds to those that were essential for trade and

long-term investment, and quashed inflation and any domestic discontent that

arose as a result. The violent suppression of the Tiananmen protests in 1989

showed that there would be no Solidarity in China.

In economic terms, China’s was the strategy that the Europeans

and Japanese had successfully used in the 1950s and 1960s. Not for nothing did

economists dub the

new configuration a “revived Bretton Woods.” The difference was that whereas the

Germans and Japanese were aligned members of America’s Cold War power bloc,

China in the new millennium was not.

For American consumers, this latest iteration of the dollar world

meant cheap imports. Wall Street made fat fees on the capital flow. American

workers in manufacturing faced fierce competition. Not that the United States

was the only economy hit by the “China shock.” European imports from China

surged, too. What the China shock exposed was the degree to which the

countervailing force of organized labor that had limited inequality in the

United States in the wake of the New Deal and World War II had, since the 1970s,

been disempowered. If Bretton Woods 1.0 had been the counterpart to the “Great

Society,” Bretton Woods 2.0 put the cap on an era of massive social

polarization. By contrast, Europe’s welfare states to a considerable extent

cushioned the China shock.

This is all the more striking because it coincided in Europe with

the move to the formation of a hard currency euro bloc. After a brief period of

uncertainty following its inauguration in January 1999, the euro soared against

the dollar from a low of less than 86 cents in September 2000 to a high seven

years later of almost $1.60.

From its original conception, one of the purposes of the euro was

to provide an alternative to the dollar as a key currency. And in the early

2000s, it seemed to be gaining real momentum. By 2007, the euro was beginning to

rival the dollar as a currency for foreign currency-denominated debt issuance.

With America bogged down in Iraq and Afghanistan and huge deficits both in

government budget and trade, it seemed that we were returning to the script of

the 1970s and the inevitable demise of the dollar under the burden of

overstretched empire.

The

meltdown arrived on cue in 2008, but it was not the one expected. It was not

a crisis of U.S. public debt and the dollar but of the entire North Atlantic

banking system, both American and European. Bankers in London, Paris,

Frankfurt, and the Netherlands had all, it turned out, wanted a piece of the

U.S. mortgage boom. Large parts of their balance sheets were denominated in

dollars. Now they all needed dollar credit. Rather than overturning the

dollar-based global financial system, the 2008 crisis exposed a profound

dependence on America.

The Fed did its best to support the trans-Atlantic banking system

by pumping dollar liquidity both to European and Asian banks in New York and to

their central banks by way of liquidity swap lines. But this could not stave off

Europe’s spiraling crisis. The euro area slid into a full-blown sovereign debt

crisis. Whereas America’s federal government balance sheet stood strong during

the crisis—U.S. sovereign debt was a safe haven, despite congressional

shenanigans and a federal shutdown—Europe was menaced by so-called doom loops,

in which ailing banks dragged down government credit ratings, which left the

state unable to support the financial system. Global confidence in the euro

collapsed.

Worldwide, the Fed’s crisis interventions under Ben Bernanke and

Janet Yellen meant dollar liquidity swamped the entire world. Dollar borrowing

surged. Not so much by large emerging market governments—the likes of Indonesia

or Thailand—that had learned their lessons and borrowed in their own currency

but by corporations and governments in so-called frontier markets. In

sub-Saharan Africa, a new era of dollar borrowing began. And the new lure of the

dollar extended even to China.

The story that was front and center in the new millennium was the

rise of China as a new superpower. And Beijing had ambitions for the yuan, too.

With the help of British Prime Minister David Cameron’s government, Beijing

embarked on an ambitious push to internationalize the Chinese currency. Perhaps

London could do for the yuan in the 2010s what it had done for the eurodollar in

the 1960s. Yet these hopes ignored the fact that Chinese business was also

internationalizing at the same time—but in the opposite direction. It was

becoming enmeshed in the dollar system.

Perhaps London could do for the yuan in the 2010s what it had

done for the eurodollar in the 1960s.

This became apparent in 2015, when China suffered the first

homegrown financial crisis of the new era. As the Shanghai stock market sold off

and the yuan slipped against the dollar, Chinese corporations desperately tried

to reduce their dollar debts. The U.S. Federal Reserve, under Yellen, helped by

postponing an increase in interest rates. Beijing, for its part, tightened

capital controls. Balance of payments liberalization and unrestricted

convertibility were off the agenda. And rather than protesting at China’s

financial repression, the world heaved a sigh of collective relief. In financial

matters, it turned out that for Beijing to be a responsible stakeholder, it did

not mean allowing trillions of dollars in Chinese funds to swash across

financial exchanges. Today, Beijing pegs to a basket of currencies rather than

the dollar alone, but its unilaterally declared Bretton Woods 2.0 continues to

have its attractions.

Meanwhile, China’s growth continues. And with every passing year,

its weight in key markets increases. For commodities such as oil, it is by far

the largest growth market. In 2018, it created a yuan-based futures contract,

which amid the gyrations in dollar-priced oil markets in the spring of 2020

proved its worth as a safe haven. In Shanghai, the price of oil never went

negative. Meanwhile, foreign investors are ever more attracted to the interest

rates on offer on Chinese bonds. Almost 10

percent of China’s sovereign bonds are now

foreign-owned. That share will increase as the bonds are included in the main

indices. But this is welcome diversification rather than an immediate threat to

dollar hegemony.

When Trump took office, there was real fear in international

financial circles that his brand of politics would be incompatible with

America’s superintendence of the global financial system. Would a Trump White

House and Republican-led Congress permit America to sustain the safety net for

the global dollar-based financial system, ultimately underpinned by the United

States? As it turned out, Trump was a president who liked a soft dollar and low

interest rates. He gave not a damn for fiscal or monetary propriety. All he

asked of the Fed was that it keep the taps open. When, in March 2020, the Fed

embarked on quantitative easing, slashed rates, and reactivated the swap lines,

Trump applauded. Soon, cronies such as Turkish President Recep Tayyip Erdogan

were pleading to be included in the Fed’s programs. The Fed did not oblige,

though as a gesture it opened a so-called repo facility for foreign reserve

holders to swap their U.S. Treasurys for cash.

And so

the ramshackle rule of the dollar has not just survived the 2020 crisis but

been reaffirmed. Can it continue?

Faced with the grandiose spectacle of China’s return to global

power, the conversation turns to history. Grand strategists invoke the

Thucydides trap and predict war. That ought to be unthinkable. But war is, in

fact, the only model we have in the modern era of a transition in hegemonic

currency. It was World War I and World War II that exploded Britain’s global

empire and brought about the dominance of the dollar. When advocates of monetary

reform on both the left and right invoke a new Bretton Woods, it is worth

remembering that the conference met in the weeks after D-Day and as the Red Army

was battering its way toward Poland. If that is our future, the question of

currency standards will be the least of our problems.

War is, in fact, the only model we have in the modern era of a

transition in hegemonic currency

If we imagine instead a more gradual transition, the key issue to

watch is the ability of the United States to attract investors willing to lend

to it in dollars. Foreign demand for U.S. Treasurys waxes and wanes with

relative interest rates and the costs of hedging the exchange rate. In recent

years, net foreign purchases of U.S. Treasurys have slowed dramatically. The

vast increase in debt driven by the COVID-19 pandemic has been absorbed by

U.S.

investors and the Fed. There was a dangerous wobble in the U.S. Treasury market

in March 2020. But that was due not to a flight out of dollars but the opposite.

Too many investors needed to access their U.S. Treasury piggy bank at once. Even

Wall Street’s über-sophisticated market makers could not absorb the sudden

sales. Reform of the financial system’s plumbing—to ensure that the market for Treasurys can smoothly absorb the trillions of dollars of new issuance that will

follow in the aftermath of the pandemic—should be an urgent priority for the

incoming administration of Joe Biden.

Both Beijing and Brussels have what it takes to develop similarly

deep asset markets. Europe’s fiscal pact for the first time promises the

creation of a substantial pool of joint European debt. But the European Union is

decades away from being able to rival the U.S. Treasury market for scale.

This does not, however, mean that the system is static. The

balance in the global economy is shifting toward Asia. A green energy revolution

would upend the global market for oil, gas, and coal. One can imagine digital

platforms beginning to operate non-state-based currencies of one form or

another, which is why central banks have been paying more and more attention to

these media of exchange and stores of value. In digital currencies, the People’s

Bank of China is leading the way.hh

In such a multipolar world, in which large parts of economic

activity may well remain

internal to each of the main blocs, one can imagine the dollar continuing

to play a

predominant role in international trade and finance.

Plausible long-range predictions out to 2050 suggest that China’s

share of global GDP will likely settle at around 20 percent, compared with

somewhere between 12 and 15 percent for the United States, EU, and India. In

such a multipolar world, in which large parts of economic activity may well

remain internal to each of the main blocs, one can imagine the dollar continuing

to play a predominant role in international trade and finance. It would be a

first. But then every successive stage in our monetary and financial history

since the advent of the modern world economy in the 19th century has been a

first. The London-centered gold standard prior to 1914, the dangerous

interregnum of the interwar period, the makeshift arrangements of the post-World

War II period, the brief precarious era of Bretton Woods, the breakthrough to

fiat money in the 1970s, China’s peg of the early 2000s, the world of

quantitative easing since 2008—each of these is without precedent.

In 1973, the economist Richard N. Cooper published an essay in Foreign

Policy offering “an unconditional forecast about the future of the dollar

for, say, the next decade.” He predicted: “At the end of a decade the position

of the dollar will not be very different from what it is now. The dollar will

continue to be suspect and the struggle to find acceptable ways to rein it in

will continue, but generally they will fail, and the dollar will still be widely

used both as a private international and as an official reserve currency. …Almost half a century later, Cooper’s forecast still seems like a

good bet. The dollar is a bit like democracy: It is the worst global currency,

except for all the others.

Almost half a century later, Cooper’s forecast still seems like a

good bet. The dollar is a bit like democracy: It is the worst global currency,

except for all the others.

The basic reason for this forecast is simple: there ' s:

The basic reason for this forecast is simple: there is at present no clear,

feasible alternative.”