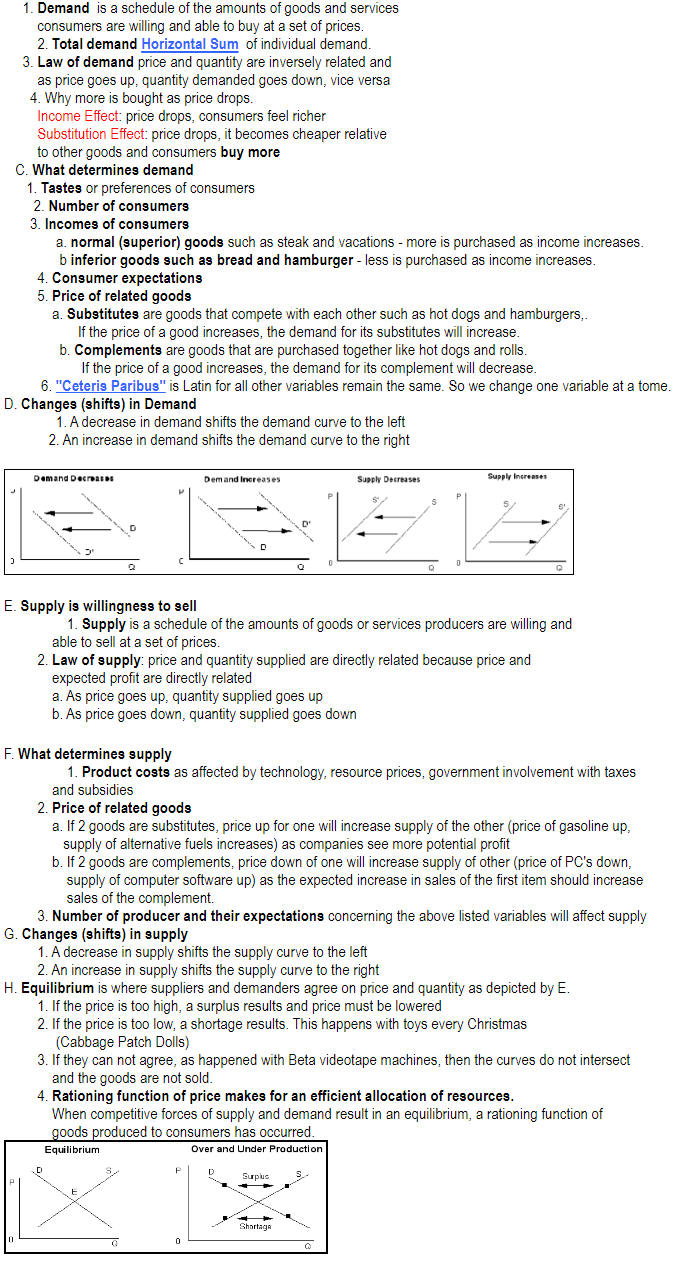

Demand and Supply Review

Chapter 4